Showing posts with label china pmi. Show all posts

Showing posts with label china pmi. Show all posts

Monday, June 6, 2011

Top 5 Graphs: Aussie GDP, U.S. and China PMI, Monetary Policy

This week we start by checking out a dismal Q1 GDP result for Australia. Then we examine the slight fall in China's manufacturing PMI (purchasing manager index), as well as the U.S. manufacturing PMI shocker. Following that is a quick check in on US consumer confidence and housing market. Finally a review of some monetary policy decisions over the past week is checked out, before the flurry of policy activity due next week.

Friday, May 6, 2011

Top 5 Economics Graphs of the Week - 7 May 2011

This week we take a look at the Purchasing Manager Index data for the US and China. Then there's a review of the US employment report, before an overview of the employment data from New Zealand, we then wrap up with a review of some of the key monetary policy decisions over the past week.

1. US PMI

The US recorded some relatively disappointing numbers, with the manufacturing PMI falling to 60.4 from 61.2 and the non-manufacturing PMI falling to 52.8 from 57.3. Sure both numbers were still in positive territory, and both still in the expansionary indicator space. But much of the weakness was in the wrong spots, e.g. things like non-manufacturing PMI falling -11.4 points, and new export orders also falling -5.5 points and business activity -6 points. While the manufacturing index saw negatives in production -5.2 points and -1.6 on new orders. However within the manufacturing PMI, there was a 8.5 point increase in backlogs and a 6 point increase in new export orders which are both interesting positives that should point to at least a short term continuation of momentum in manufacturing.

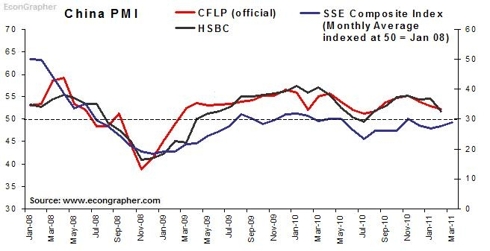

2. China PMI

The official CFLP manufacturing PMI came in at 52.9 in April, down slightly from 53.4 in March, and below the Bloomberg consensus of 53.9. The preliminary HSBC/Markit reading was 51.8, the same as the March reading. The readings show the manufacturing sector in China still in expansionary mode, which bodes well for the Chinese economy. But it could well herald another move by the People's Bank of China, particularly given recent comments that it will continue to fight inflation. Next week is China's monthly data release, where inflation is likely to moderate compared to March's 5.4% reading, but it could be an opportune time for the People's Bank of China to do one last interest rate increase.

3. US Nonfarm Payrolls

The US added 244k nonfarm payrolls in April, up slightly versus March's 221k, and compares to 277k in April 2010. The figure brings 2011 net new nonfarm payrolls to 768k YTD. Less meaningfully, the unemployment rate rose slightly to 9.0% from 8.8% in March. So, all up it was a reasonably positive result. The US economy is finally starting to see consistency in jobs added, and this area will likely be a key aspect for a recovery in consumer spending, and thus a key factor in the housing market, as well as general inflation levels. It's likely that job growth will continue to expand in the months ahead, but as identified in the PMI results, there are due downside risks to the US economy, and an early peak in the PMI could well be negative for the jobs outlook.

4. New Zealand Employment Data

New Zealand reported a 30k increase in jobs through the first quarter of this year, with 20k being part time jobs and 10k being full time. The unemployment rate eased slightly to 6.6%, down from 6.7% in Q4 2010, and off of the peak of 7% in Q4 2009. The employment picture in New Zealand is slowly improving, albeit with the negative contribution from the Christchurch earthquake. But with the rugby world cup event soon approaching there should be a noticeable pick up in part-time jobs, at least in the medium term. After that it's more about how the broader economy can gain momentum and leverage off loose monetary policy, high terms of trade, and one-off boosts. The downside is the need for fiscal tightening, with the government likely to announce a more prudent budget in the next couple of weeks as it seeks to sure up government finances and maintain its AA+ credit rating.

5. Monetary Policy Review

On the monetary policy front, the past week was characterized by continued emerging market policy tightening, and continued developed market policy caution. Of the central banks that made decisions on monetary policy settings this week, those that increased were: India +50bps to 7.25%, Philippines +25bps to 4.50%, and Malaysia +25bps to 3.00%. Meanwhile those that held rates were: Australia 4.75%, Romania 6.25%, United Kingdom 0.50%, European Union 1.25%, and the Czech Republic 0.75%. Next week there's interest rate decisions from Poland (11 May) currently 4.00% , Norway (12th May) currently 2.00%, South Africa (12th) currently 5.50%, and South Korea (13th May) currently 3.00%. Most of these banks will probably increase or maintain a hawkish stance.

Summary

So we saw some relatively disappointing PMI results from the US, but with some glimmers of strength still showing through in the manufacturing index. Over in China there was a slight weakening, but generally things were still strong - perhaps allowing scope for another interest rate increase. Meanwhile the US reported a good nonfarm payrolls figure in April, with some promise for continued strength. Over to New Zealand, the March quarter saw a decent employment report, with a positive outlook as the New Zealand economy looks set to gain momentum. On monetary policy the theme of emerging market tightening continued, and is likely to continue for the time being, meanwhile the overriding theme for developed market central banks was policy caution.

Sources

1. US Institute for Supply Management www.ism.ws & Yahoo Finance finance.yahoo.com

2. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

3. Bureau of Labour Statistics www.bls.gov

4. Statistics New Zealand www.stats.govt.nz

5. CentralBankNews.info www.centralbanknews.info

Article Source: http://www.econgrapher.com/top5graphs7may11.html

1. US PMI

The US recorded some relatively disappointing numbers, with the manufacturing PMI falling to 60.4 from 61.2 and the non-manufacturing PMI falling to 52.8 from 57.3. Sure both numbers were still in positive territory, and both still in the expansionary indicator space. But much of the weakness was in the wrong spots, e.g. things like non-manufacturing PMI falling -11.4 points, and new export orders also falling -5.5 points and business activity -6 points. While the manufacturing index saw negatives in production -5.2 points and -1.6 on new orders. However within the manufacturing PMI, there was a 8.5 point increase in backlogs and a 6 point increase in new export orders which are both interesting positives that should point to at least a short term continuation of momentum in manufacturing.

2. China PMI

The official CFLP manufacturing PMI came in at 52.9 in April, down slightly from 53.4 in March, and below the Bloomberg consensus of 53.9. The preliminary HSBC/Markit reading was 51.8, the same as the March reading. The readings show the manufacturing sector in China still in expansionary mode, which bodes well for the Chinese economy. But it could well herald another move by the People's Bank of China, particularly given recent comments that it will continue to fight inflation. Next week is China's monthly data release, where inflation is likely to moderate compared to March's 5.4% reading, but it could be an opportune time for the People's Bank of China to do one last interest rate increase.

3. US Nonfarm Payrolls

The US added 244k nonfarm payrolls in April, up slightly versus March's 221k, and compares to 277k in April 2010. The figure brings 2011 net new nonfarm payrolls to 768k YTD. Less meaningfully, the unemployment rate rose slightly to 9.0% from 8.8% in March. So, all up it was a reasonably positive result. The US economy is finally starting to see consistency in jobs added, and this area will likely be a key aspect for a recovery in consumer spending, and thus a key factor in the housing market, as well as general inflation levels. It's likely that job growth will continue to expand in the months ahead, but as identified in the PMI results, there are due downside risks to the US economy, and an early peak in the PMI could well be negative for the jobs outlook.

4. New Zealand Employment Data

New Zealand reported a 30k increase in jobs through the first quarter of this year, with 20k being part time jobs and 10k being full time. The unemployment rate eased slightly to 6.6%, down from 6.7% in Q4 2010, and off of the peak of 7% in Q4 2009. The employment picture in New Zealand is slowly improving, albeit with the negative contribution from the Christchurch earthquake. But with the rugby world cup event soon approaching there should be a noticeable pick up in part-time jobs, at least in the medium term. After that it's more about how the broader economy can gain momentum and leverage off loose monetary policy, high terms of trade, and one-off boosts. The downside is the need for fiscal tightening, with the government likely to announce a more prudent budget in the next couple of weeks as it seeks to sure up government finances and maintain its AA+ credit rating.

5. Monetary Policy Review

On the monetary policy front, the past week was characterized by continued emerging market policy tightening, and continued developed market policy caution. Of the central banks that made decisions on monetary policy settings this week, those that increased were: India +50bps to 7.25%, Philippines +25bps to 4.50%, and Malaysia +25bps to 3.00%. Meanwhile those that held rates were: Australia 4.75%, Romania 6.25%, United Kingdom 0.50%, European Union 1.25%, and the Czech Republic 0.75%. Next week there's interest rate decisions from Poland (11 May) currently 4.00% , Norway (12th May) currently 2.00%, South Africa (12th) currently 5.50%, and South Korea (13th May) currently 3.00%. Most of these banks will probably increase or maintain a hawkish stance.

Summary

So we saw some relatively disappointing PMI results from the US, but with some glimmers of strength still showing through in the manufacturing index. Over in China there was a slight weakening, but generally things were still strong - perhaps allowing scope for another interest rate increase. Meanwhile the US reported a good nonfarm payrolls figure in April, with some promise for continued strength. Over to New Zealand, the March quarter saw a decent employment report, with a positive outlook as the New Zealand economy looks set to gain momentum. On monetary policy the theme of emerging market tightening continued, and is likely to continue for the time being, meanwhile the overriding theme for developed market central banks was policy caution.

Sources

1. US Institute for Supply Management www.ism.ws & Yahoo Finance finance.yahoo.com

2. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

3. Bureau of Labour Statistics www.bls.gov

4. Statistics New Zealand www.stats.govt.nz

5. CentralBankNews.info www.centralbanknews.info

Article Source: http://www.econgrapher.com/top5graphs7may11.html

Monday, May 2, 2011

China PMI Heralds Further Policy Tightening and Possible Opportunities

China's April PMI stats just came out and were more or less flat compared to March. The official CFLP manufacturing PMI came in at 52.9 in April, down slightly from 53.4 in March, and below the Bloomberg consensus of 53.9. The preliminary HSBC/Markit reading was 51.8, the same as the March reading. The readings show the manufacturing sector in China still in expansionary mode, which bodes well for the Chinese economy. Paradoxically perhaps, in the short term it will likely mean further monetary policy tightening with an increasing likelihood of an additional interest rate hike as the economy proves relatively resilient to the inflation fighting efforts to date.

http://seekingalpha.com/article/267013-china-pmi-heralds-further-policy-tightening-and-possible-opportunities

http://seekingalpha.com/article/267013-china-pmi-heralds-further-policy-tightening-and-possible-opportunities

Saturday, March 5, 2011

Top 5 Economics Graphs of the Week - 6 Mar 2011

This week we look at the PMI results from the US and China, with some similar patterns and interesting conclusions. Then we review Australian GDP, finding some mixed signals, followed by a look at the recent US nonfarm payrolls report. Finally we wrap up with a review of some particularly interesting monetary policy decisions over the past week.

1. China PMI

China's February PMI readings showed a few seasonal quirks, but also pointed to rising inflationary pressures. The official CFLP PMI was 52.2 vs 52.9 prev, and the HSBC index was 51.7 vs 54.5. Though both indexes fell, they remained above 50 and generally did not point to any significant slowdown. The key warning signal that did come out of the numbers was for further upside inflation risks. The HSBC "Input Prices" sub-index came in at 74.6 vs 71 in January, as rising commodity prices put increasing upward pressure on prices in China and other emerging markets. The HSBC index also showed a rise in the backlogs of work, with rising capacity constraints showing through.

2. US PMI

The U.S. impressed once again with its manufacturing Purchasing Managers Index results. The main PMI index crept up a further 0.6 to 61.4, the highest level since the early 1980's. New orders added 0.2 to 68.0 and the employment sub-index added 2.8 to 64.5 as more employers signaled higher staff (a net 26% expect higher employment). On the non-manufacturing side, the NMI rose to 59.7 from 59.4, with the standouts being business activity +2.3, inventories +6.5, and most interestingly, new export orders +3 points to 56.5 (compared to the imports index at 53.4). Both indexes signalled rising cost pressures with the NMI prices sub-index up 1.2 to 73.3, and the PMI prices sub-index up 0.5 to 82 - showing that inflation is not dead.ff

3. Australian GDP

The Australian economy produced a solid yet uninspiring GDP result for the final quarter of 2010. The Aussie economy expanded at a q/q growth rate of +0.7% (or 2.8% annualized), placing y/y growth at +2.7%. The majority of the growth came from inventory-building, with net exports neutral, and an insipid contribution from consumption. Thus the Australian economy appears to be passing through the hard part of its recession-free recovery. The outlook for the Australian economy is relatively strong growth - perhaps about 3%, and it's likely that any further tightening from the RBA will be pushed out well into the second half of this year.

4. US Nonfarm payrolls

The US recorded a bumper month, by recent standards, in February with 192k jobs added (compared to 36k in January). Private payrolls were up 222k, compared to 50k in Jan. The unemployment rate fell slightly to 8.9% - which is not that meaningful in the scheme of things. Average hourly earnings were flat, as was the average workweek. Thus overall it was a decent result in terms of the number of jobs added, sure some of it was January hiring being pushed into Feb, but a few more months like this would start to make a difference. As it stands, payrolls are still down a net -7.47 million since the start of 2008, so yeah, still a long way to go (oh and since January 2000, payrolls are net negative by about 30k, so who knows - next month could mark the start of a net positive number!).

5. Monetary Policy

In monetary policy the main standout for the week had to be the ECB's tough talking, and rhetoric that hinted at an impending rate hike - perhaps as soon as April. The other big one was Brazil tightening another 50bps, sending the Selic rate to 11.75% as it seeks to rein in rising inflation. Likewise Azerbaijan +200bps, Tajikistan +75bps, and the Dominican Republic +100bps also lifted rates to stave off rising inflation, driven by a spike in food and energy prices. So the usual theme of rising commodity prices and emerging market inflation was highlighted again - but the interesting part was the developed markets story. The European Central Bank specifically noted its concerns about the second round effects of rising commodity prices; so again, inflation is not dead...

Summary

So we saw China put out lower PMI figures, pointing to what will most likely be a temporary tapering off of activity, but more importantly; signaling rising inflationary pressures. Over to the US there was a much more positive PMI result, with some promising signs of strength in activity levels, but the costs pressures signals were also there. In Australia the economy is chugging along as per usual, though the 2010 Q4 results, though positive, were a little less inspiring. Back to the US, the February payrolls figure was a strong one, but there's still a lot more work to be done to get back even close to normal. Meanwhile in monetary policy, the ECB sent strong signals about and impending rate hike, and emerging markets, including one of the BRIC economies, continued to lift interest rates in response to their not-so-unique rising inflationary pressures situation.

Sources

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Institute for Supply Management www.ism.ws

3. Australian Bureau of Statistics www.abs.gov.au

4. Bureau of Labor Statistics www.bls.gov

5. CentralBankNews.info www.centralbanknews.info

Article Source: http://www.econgrapher.com/top5graphs6mar11.html

1. China PMI

China's February PMI readings showed a few seasonal quirks, but also pointed to rising inflationary pressures. The official CFLP PMI was 52.2 vs 52.9 prev, and the HSBC index was 51.7 vs 54.5. Though both indexes fell, they remained above 50 and generally did not point to any significant slowdown. The key warning signal that did come out of the numbers was for further upside inflation risks. The HSBC "Input Prices" sub-index came in at 74.6 vs 71 in January, as rising commodity prices put increasing upward pressure on prices in China and other emerging markets. The HSBC index also showed a rise in the backlogs of work, with rising capacity constraints showing through.

2. US PMI

The U.S. impressed once again with its manufacturing Purchasing Managers Index results. The main PMI index crept up a further 0.6 to 61.4, the highest level since the early 1980's. New orders added 0.2 to 68.0 and the employment sub-index added 2.8 to 64.5 as more employers signaled higher staff (a net 26% expect higher employment). On the non-manufacturing side, the NMI rose to 59.7 from 59.4, with the standouts being business activity +2.3, inventories +6.5, and most interestingly, new export orders +3 points to 56.5 (compared to the imports index at 53.4). Both indexes signalled rising cost pressures with the NMI prices sub-index up 1.2 to 73.3, and the PMI prices sub-index up 0.5 to 82 - showing that inflation is not dead.ff

3. Australian GDP

The Australian economy produced a solid yet uninspiring GDP result for the final quarter of 2010. The Aussie economy expanded at a q/q growth rate of +0.7% (or 2.8% annualized), placing y/y growth at +2.7%. The majority of the growth came from inventory-building, with net exports neutral, and an insipid contribution from consumption. Thus the Australian economy appears to be passing through the hard part of its recession-free recovery. The outlook for the Australian economy is relatively strong growth - perhaps about 3%, and it's likely that any further tightening from the RBA will be pushed out well into the second half of this year.

4. US Nonfarm payrolls

The US recorded a bumper month, by recent standards, in February with 192k jobs added (compared to 36k in January). Private payrolls were up 222k, compared to 50k in Jan. The unemployment rate fell slightly to 8.9% - which is not that meaningful in the scheme of things. Average hourly earnings were flat, as was the average workweek. Thus overall it was a decent result in terms of the number of jobs added, sure some of it was January hiring being pushed into Feb, but a few more months like this would start to make a difference. As it stands, payrolls are still down a net -7.47 million since the start of 2008, so yeah, still a long way to go (oh and since January 2000, payrolls are net negative by about 30k, so who knows - next month could mark the start of a net positive number!).

5. Monetary Policy

In monetary policy the main standout for the week had to be the ECB's tough talking, and rhetoric that hinted at an impending rate hike - perhaps as soon as April. The other big one was Brazil tightening another 50bps, sending the Selic rate to 11.75% as it seeks to rein in rising inflation. Likewise Azerbaijan +200bps, Tajikistan +75bps, and the Dominican Republic +100bps also lifted rates to stave off rising inflation, driven by a spike in food and energy prices. So the usual theme of rising commodity prices and emerging market inflation was highlighted again - but the interesting part was the developed markets story. The European Central Bank specifically noted its concerns about the second round effects of rising commodity prices; so again, inflation is not dead...

Summary

So we saw China put out lower PMI figures, pointing to what will most likely be a temporary tapering off of activity, but more importantly; signaling rising inflationary pressures. Over to the US there was a much more positive PMI result, with some promising signs of strength in activity levels, but the costs pressures signals were also there. In Australia the economy is chugging along as per usual, though the 2010 Q4 results, though positive, were a little less inspiring. Back to the US, the February payrolls figure was a strong one, but there's still a lot more work to be done to get back even close to normal. Meanwhile in monetary policy, the ECB sent strong signals about and impending rate hike, and emerging markets, including one of the BRIC economies, continued to lift interest rates in response to their not-so-unique rising inflationary pressures situation.

Sources

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Institute for Supply Management www.ism.ws

3. Australian Bureau of Statistics www.abs.gov.au

4. Bureau of Labor Statistics www.bls.gov

5. CentralBankNews.info www.centralbanknews.info

Article Source: http://www.econgrapher.com/top5graphs6mar11.html

Tuesday, March 1, 2011

China PMI Points to Rising Inflation Risks

China Just saw the release of its two PMI indexes for February; the official CFLP (52.2 vs 52.9 prev), and the HSBC (51.7 vs 54.5). Though both indexes fell, they remained above 50 and generally did not point to any significant slowdown. But the warning signal that did come out of the numbers was for further upside inflation risks.

http://seekingalpha.com/article/255653-china-pmi-points-to-rising-inflation-risks

http://seekingalpha.com/article/255653-china-pmi-points-to-rising-inflation-risks

Saturday, January 1, 2011

Top 5 Economics Graphs of the Week - 1 Jan 2011

This week we look at China PMI, US house prices, US consumer confidence, French GDP results, and Japan's unemployment and inflation situation.

1. China PMI

China recorded slightly lower PMI figures for December with the HSBC index falling to 54.4 from 55.3 and the CFLP index falling to 53.9 from 55.2. Clearly there are a few issues bubbling away i.e. a spike in inflation... and more importantly - how the authorities deal with it. That alone will be one of the biggest wild-cards for 2011.

2. US Housing

The US housing market saw further weakness with the October reading of the Case-Shiller index down both on a monthly and annual basis. There's not much else to say on this one, house prices ran ahead of themselves and the market needs to correct - further government measures may put a temporary floor under the market, but the question is how long would that be necessary before the fundamentals finally came around? Another couple of years of flat house prices wouldn't be a surprise.

3. US Confidence

US Consumer Confidence dipped slightly in December, dropping to 52.5 from 54.1, with the weakness being expressed in both the current conditions and futures expectations indexes. Similar story to the housing market really - when will the key fundamentals turnaround? High unemployment and stagnant house prices will continue to weigh on this one in the medium term.

4. France GDP

France saw its economy expand 0.3% q/q vs 0.6% in Q2, with some minor downward revisions. Net exports made a negative contribution, household consumption and government consumption both made a positive contribution. Most are forecasting about 0.4% GDP growth in Q4. So it's chugging along OK for the French economy, not as fast as the Germans, but they're getting there.

5. Japan unemployment and inflation

Japan saw another month of positive inflation in November - barely, with the CPI increasing 0.1% y/y vs 0.2% in October. Meanwhile unemployment stuck around 5% with a 5.1% reading for November. Still many a challenge for Japan - but will the policy makers get it right? (for that matter what else is there left for them to do?)

Summary

So we saw China show a lower PMI figure on the back of uncertainty about the inflation battle. Over in the US there were no positive signs for the housing market in terms of prices in the near term, and consumer confidence is still low - also reflecting where fundamentals are currently at, but let's see what 2011 brings. Then we looked at France's GDP growth, and saw that they're chugging along alright out of the recession. Meanwhile in Japan there's just barely some positive inflation, and unemployment is little changed. So there you go, the first issue of 2011, may the year ahead bring you much happiness, health and success - it's sure to be an interesting year!

Sources

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Standard & Poor's www.standardandpoors.com

3. US Conference Board www.conference-board.org & US Bureau of Labor Statistics www.bls.gov

4. OECD Statistics Database stats.oecd.org/index.aspx

5. Trading Economics www.tradingeconomics.com

Article Source: http://www.econgrapher.com/top5graphs1jan11.html

1. China PMI

China recorded slightly lower PMI figures for December with the HSBC index falling to 54.4 from 55.3 and the CFLP index falling to 53.9 from 55.2. Clearly there are a few issues bubbling away i.e. a spike in inflation... and more importantly - how the authorities deal with it. That alone will be one of the biggest wild-cards for 2011.

2. US Housing

The US housing market saw further weakness with the October reading of the Case-Shiller index down both on a monthly and annual basis. There's not much else to say on this one, house prices ran ahead of themselves and the market needs to correct - further government measures may put a temporary floor under the market, but the question is how long would that be necessary before the fundamentals finally came around? Another couple of years of flat house prices wouldn't be a surprise.

3. US Confidence

US Consumer Confidence dipped slightly in December, dropping to 52.5 from 54.1, with the weakness being expressed in both the current conditions and futures expectations indexes. Similar story to the housing market really - when will the key fundamentals turnaround? High unemployment and stagnant house prices will continue to weigh on this one in the medium term.

4. France GDP

France saw its economy expand 0.3% q/q vs 0.6% in Q2, with some minor downward revisions. Net exports made a negative contribution, household consumption and government consumption both made a positive contribution. Most are forecasting about 0.4% GDP growth in Q4. So it's chugging along OK for the French economy, not as fast as the Germans, but they're getting there.

5. Japan unemployment and inflation

Japan saw another month of positive inflation in November - barely, with the CPI increasing 0.1% y/y vs 0.2% in October. Meanwhile unemployment stuck around 5% with a 5.1% reading for November. Still many a challenge for Japan - but will the policy makers get it right? (for that matter what else is there left for them to do?)

Summary

So we saw China show a lower PMI figure on the back of uncertainty about the inflation battle. Over in the US there were no positive signs for the housing market in terms of prices in the near term, and consumer confidence is still low - also reflecting where fundamentals are currently at, but let's see what 2011 brings. Then we looked at France's GDP growth, and saw that they're chugging along alright out of the recession. Meanwhile in Japan there's just barely some positive inflation, and unemployment is little changed. So there you go, the first issue of 2011, may the year ahead bring you much happiness, health and success - it's sure to be an interesting year!

Sources

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Standard & Poor's www.standardandpoors.com

3. US Conference Board www.conference-board.org & US Bureau of Labor Statistics www.bls.gov

4. OECD Statistics Database stats.oecd.org/index.aspx

5. Trading Economics www.tradingeconomics.com

Article Source: http://www.econgrapher.com/top5graphs1jan11.html

Friday, December 3, 2010

Top 5 Economics Graphs of the Week - 4 December 2010

This week we look at the US PMI results; while also reviewing the China PMI data for November. Then we check out the 3rd quarter GDP results for Australia, before wrapping up with a closer look at some US data on the housing market, consumer confidence, and the nonfarm payrolls report.

1. US PMI

The US manufacturing PMI came in at 56.6, a little below consensus 57 and previous 56.9, the non-manufacturing PMI matched consensus at 55.0, and increased vs October's 54.3 reading. So between manufacturing and services there was a bit of variation, also within the results the manufacturing sub-components were not great e.g. falls in new orders, production, employment, exports. But within the services sub-indices there was a bit more positives e.g. rises in new orders, new export orders, employment, etc. So overall the results are generally positive, and not really surprising given where the US economy is at.

2. China PMI

Over to China, the official PMI rose to 55.2 from 54.7 in October; beyond expectations for 54.8. The HSBC Markit index rose to an 8 month high of 55.3 from 54.8 in October. The standouts in the sub-indices were Production (58.5 vs 57.1), Supplier Delivery (48.9 vs 49.3), New Orders was basically flat, but still strong (58.3 vs 58.2), similarly Employees was little changed (52.0 vs 52.1). In general its good to see the index rising, its also positive to see it still in the expansionary zone, and it will give comfort to those watching China's attempt at a managed slowdown as inflation pressures rise.

3. Australia GDP

The Australian economy grew 0.20% q/q in the September quarter, placing Australian GDP up 2.7% year on year. The pace of growth was slower than the expected 0.40% q/q growth, as global volatility, exchange rate pressures on exports, and withdrawal of fiscal stimulus measures took their toll on the Australian economy. Looking forward though the pace of growth is likely to rebound in 2011 as the resources sector surges ahead with a number of large scale mining projects in the pipeline, and farming continues to contribute; and of course the flow on effects to the rest of the economy.

4. US House Prices and Confidence

Two key pieces of data release last week were the Case-Shiller house price index, which showed house prices falling further (no surprise). The other key data point was the Conference Board Consumer Confidence index, which showed a jump to 54.1 (vs consensus 52, previous 50.2). Within the confidence numbers, the present situation index rose to 24 from 23.5 and the expectations index jumped to 74.2 from 67.5 previously. So people are feeling a little better about the future, but just not so much about the here and now. And looking to the housing market, the future may be better, but the short-medium term probably has further downside risk unless the fundamentals sharply turnaround.

5. US Nonfarm Payrolls

The US added 39k nonfarm payrolls in November, vs 151k in October, and well below consensus 168k. Private payrolls were up 50k vs 159k in October. Average hourly earnings were flat, as was the average work week. So overall not a great result, good that it was positive, but basically it lines up with the idea that the US recovery is not going to be linear, and basically that there is going to be choppiness as the US economy muddles through the next year or two.

Summary

So we saw the manufacturing PMI in the US still strong, but with some negatives in the sub-components, the services PMI however was a bit stronger and relatively more promising. Meanwhile in China the manufacturing PMI improved, showing that the concern is rightfully more about the risks of overheating rather than not growing. In Australia, the economy continued to grow, but a little less so as stimulus wore off, but expect the slowdown to be temporary. Back to the US, the housing market is still under the gun, but the consumer is slowly feeling a bit better about the future, in spite of the job market also remaining relatively subdued.

Sources

1. Institute for Supply Management www.ism.ws & Yahoo Finance finance.yahoo.com

2. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & National Bureau of Statistics www.stats.gov.cn

3. Australian Bureau of Statistics www.abs.gov.au

4. Conference Board www.conference-board.org & Standard & Poors www.standardandpoors.com

5. Bureau of Labour Statistics www.bls.gov

Article Source: http://www.econgrapher.com/top5graphs-4dec.html

1. US PMI

The US manufacturing PMI came in at 56.6, a little below consensus 57 and previous 56.9, the non-manufacturing PMI matched consensus at 55.0, and increased vs October's 54.3 reading. So between manufacturing and services there was a bit of variation, also within the results the manufacturing sub-components were not great e.g. falls in new orders, production, employment, exports. But within the services sub-indices there was a bit more positives e.g. rises in new orders, new export orders, employment, etc. So overall the results are generally positive, and not really surprising given where the US economy is at.

2. China PMI

Over to China, the official PMI rose to 55.2 from 54.7 in October; beyond expectations for 54.8. The HSBC Markit index rose to an 8 month high of 55.3 from 54.8 in October. The standouts in the sub-indices were Production (58.5 vs 57.1), Supplier Delivery (48.9 vs 49.3), New Orders was basically flat, but still strong (58.3 vs 58.2), similarly Employees was little changed (52.0 vs 52.1). In general its good to see the index rising, its also positive to see it still in the expansionary zone, and it will give comfort to those watching China's attempt at a managed slowdown as inflation pressures rise.

3. Australia GDP

The Australian economy grew 0.20% q/q in the September quarter, placing Australian GDP up 2.7% year on year. The pace of growth was slower than the expected 0.40% q/q growth, as global volatility, exchange rate pressures on exports, and withdrawal of fiscal stimulus measures took their toll on the Australian economy. Looking forward though the pace of growth is likely to rebound in 2011 as the resources sector surges ahead with a number of large scale mining projects in the pipeline, and farming continues to contribute; and of course the flow on effects to the rest of the economy.

4. US House Prices and Confidence

Two key pieces of data release last week were the Case-Shiller house price index, which showed house prices falling further (no surprise). The other key data point was the Conference Board Consumer Confidence index, which showed a jump to 54.1 (vs consensus 52, previous 50.2). Within the confidence numbers, the present situation index rose to 24 from 23.5 and the expectations index jumped to 74.2 from 67.5 previously. So people are feeling a little better about the future, but just not so much about the here and now. And looking to the housing market, the future may be better, but the short-medium term probably has further downside risk unless the fundamentals sharply turnaround.

5. US Nonfarm Payrolls

The US added 39k nonfarm payrolls in November, vs 151k in October, and well below consensus 168k. Private payrolls were up 50k vs 159k in October. Average hourly earnings were flat, as was the average work week. So overall not a great result, good that it was positive, but basically it lines up with the idea that the US recovery is not going to be linear, and basically that there is going to be choppiness as the US economy muddles through the next year or two.

Summary

So we saw the manufacturing PMI in the US still strong, but with some negatives in the sub-components, the services PMI however was a bit stronger and relatively more promising. Meanwhile in China the manufacturing PMI improved, showing that the concern is rightfully more about the risks of overheating rather than not growing. In Australia, the economy continued to grow, but a little less so as stimulus wore off, but expect the slowdown to be temporary. Back to the US, the housing market is still under the gun, but the consumer is slowly feeling a bit better about the future, in spite of the job market also remaining relatively subdued.

Sources

1. Institute for Supply Management www.ism.ws & Yahoo Finance finance.yahoo.com

2. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & National Bureau of Statistics www.stats.gov.cn

3. Australian Bureau of Statistics www.abs.gov.au

4. Conference Board www.conference-board.org & Standard & Poors www.standardandpoors.com

5. Bureau of Labour Statistics www.bls.gov

Article Source: http://www.econgrapher.com/top5graphs-4dec.html

Thursday, December 2, 2010

US & China PMI Review

Both China and the US released their November PMI stats in the past few days, showing relatively strong vitals in both of their manufacturing sectors. Looking first at China, the official PMI rose to 55.2 from 54.7 in October; beyond expectations for 54.8. The HSBC Markit index rose to an 8 month high of 55.3 from 54.8 in October. The standouts in the sub-indices were Production (58.5 vs 57.1), Supplier Delivery (48.9 vs 49.3), New Orders was basically flat, but still strong (58.3 vs 58.2), similarly Employees was little changed (52.0 vs 52.1).

So overall a relatively strong result from China, new orders are still going strong, production activity is picking up, which is all a positive sign given the moves the authorities have taken to tackle inflation and perhaps engineer some sort of soft landing. It's a good sign, because it shows there is still solid fundamental strength in the Chinese economy, i.e. that it can withstand a bit of a slowing.

Meanwhile in the US, the ISM PMI reduced slightly to 56.6 from 56.9, and slightly below consensus 57. But again, the figure is comfortably above the 50 point mark, indicating relatively robust expansion. Looking at the detail however, much of the changes were particularly impressive, production fell off quite a bit, new orders fell, exports fell, and employment was basically flat. So we're in the right space for now, but if this sort of pattern repeats, it will be back to square one for the manufacturing sector.

So the takeaway is that the current state of the US and Chinese manufacturing sectors is relatively positive. China probably more so, and the direction is also probably more promising, and it lines up with the view that China's economy still has a decent amount of wind left in it. The US meanwhile is showing strength, but the wobbles are also showing through - there will be strength but as noted before, the US is in the muddle ages of the recovery, so it's almost certain to be a nonlinear progression.

Sources

Econ Grapher Analytics www.econgrapher.com

CFLP www.chinawuliu.com.cn

Markit/HSBC www.markiteconomics.com

Yahoo Finance finance.yahoo.com

Institute for Supply Management www.ism.ws

Article Source: http://www.econgrapher.com/2dec-uschinapmi.html

So overall a relatively strong result from China, new orders are still going strong, production activity is picking up, which is all a positive sign given the moves the authorities have taken to tackle inflation and perhaps engineer some sort of soft landing. It's a good sign, because it shows there is still solid fundamental strength in the Chinese economy, i.e. that it can withstand a bit of a slowing.

Meanwhile in the US, the ISM PMI reduced slightly to 56.6 from 56.9, and slightly below consensus 57. But again, the figure is comfortably above the 50 point mark, indicating relatively robust expansion. Looking at the detail however, much of the changes were particularly impressive, production fell off quite a bit, new orders fell, exports fell, and employment was basically flat. So we're in the right space for now, but if this sort of pattern repeats, it will be back to square one for the manufacturing sector.

So the takeaway is that the current state of the US and Chinese manufacturing sectors is relatively positive. China probably more so, and the direction is also probably more promising, and it lines up with the view that China's economy still has a decent amount of wind left in it. The US meanwhile is showing strength, but the wobbles are also showing through - there will be strength but as noted before, the US is in the muddle ages of the recovery, so it's almost certain to be a nonlinear progression.

Sources

Econ Grapher Analytics www.econgrapher.com

CFLP www.chinawuliu.com.cn

Markit/HSBC www.markiteconomics.com

Yahoo Finance finance.yahoo.com

Institute for Supply Management www.ism.ws

Article Source: http://www.econgrapher.com/2dec-uschinapmi.html

Saturday, November 27, 2010

Economic Calendar - 28 November 2010

Here's the Economic Calendar for the week commencing the 28th of November 2010. This week December starts! So the PMI data will start flowing with releases expected from China, Japan, the US, and the EU, among others. There's also some more GDP data out this week with Australia, Canada, and Switzerland announcing their Q3 results. In the US there's the S&P/Case-Shiller house price index, consumer confidence, nonfarm payrolls, and the Beige Book from the Fed.

(More commentary follows the table)

| Day | GMT | Country/ Currency | Event | Forecast | Previous |

| SUN | 21:45 | NZD | Trade Balance [New Zealand dollars] [OCT] | -400M | -532M |

| SUN | 21:45 | NZD | Exports [New Zealand dollars] [OCT] | 3.31B | 3.16B |

| SUN | 21:45 | NZD | Imports [New Zealand dollars] [OCT] | 3.78B | 3.69B |

| SUN | 23:50 | JPY | Retail Trade [YoY] [OCT] | 0.70% | 1.40% |

| SUN | 02:00 | NZD | NBNZ Business Confidence [NOV] | 23.70 | |

| MON | 10:00 | EUR | Euro-Zone Business Climate Indicator [NOV] | 1.05 | 0.98 |

| MON | 10:00 | EUR | Euro-Zone Consumer Confidence [NOV F] | -10.00 | -10.00 |

| MON | 10:00 | EUR | Euro-Zone Economic Confidence [NOV] | 105.00 | 104.10 |

| MON | 10:00 | EUR | Euro-Zone Industrial Confidence [NOV] | 2.00 | 0.00 |

| MON | 10:00 | EUR | Euro-Zone Services Confidence [NOV] | 9.00 | 8.00 |

| MON | 13:30 | CAD | Current Account [BoP] [Canadian dollar] [3Q] | -$15.2B | -$11.0B |

| MON | 23:30 | JPY | Jobless Rate [OCT] | 5.00% | 5.00% |

| MON | 23:50 | JPY | Industrial Production [MoM] [OCT P] | -3.20% | -1.60% |

| MON | 23:50 | JPY | Industrial Production [YoY] [OCT P] | 3.10% | 11.50% |

| MON | 00:30 | AUD | Current Account Balance [Australian Dollar] [3Q] | -6600M | -5640M |

| TUE | 05:00 | JPY | Housing Starts [YoY] [OCT] | 9.70% | 17.70% |

| TUE | 05:00 | JPY | Annualized Housing Starts [OCT] | 0.840M | 0.837M |

| TUE | 05:00 | JPY | Nomura/JMMA Manufacturing PMI [NOV] | 47.20 | |

| TUE | 08:55 | EUR | German Unemployment Change [NOV] | -20K | -3K |

| TUE | 10:00 | EUR | Euro-Zone CPI Estimate [YoY] [NOV] | 1.90% | 1.90% |

| TUE | 10:00 | EUR | Euro-Zone Unemployment Rate [OCT] | 10.10% | 10.10% |

| TUE | 11:00 | EUR | Italian Unemployment Rate s.a. [OCT] | 8.40% | 8.30% |

| TUE | 13:30 | CAD | Gross Domestic Product [MoM] [SEP] [SEP] | 0.10% | 0.30% |

| TUE | 13:30 | CAD | Quarterly GDP Annualized [3Q] | 1.50% | 2.00% |

| TUE | 14:00 | USD | S&P/Case-Shiller Composite-20 [YoY] [SEP] | 1.00% | 1.70% |

| TUE | 14:00 | USD | S&P/Case-Shiller US Home Price Index [YoY] | 3.60% | |

| TUE | 14:00 | USD | S&P/Case-Shiller 20 City [MoM] s.a. [SEP] | -0.40% | -0.28% |

| TUE | 15:00 | USD | Consumer Confidence [NOV] | 52.70 | 50.20 |

| TUE | 00:30 | AUD | Gross Domestic Product [QoQ] [3Q] | 0.50% | 1.20% |

| TUE | 00:30 | AUD | Gross Domestic Product [YoY] [3Q] | 3.40% | 3.30% |

| TUE | 01:00 | CNY | PMI Manufacturing [NOV] | 54.80 | 54.70 |

| TUE | 02:00 | NZD | ANZ Commodity Price [NOV] | 2.90% | |

| TUE | 02:30 | CNY | HSBC Manufacturing PMI [NOV] | 55.40 | 54.80 |

| WED | 07:00 | GBP | Nationwide House Prices n.s.a. [YoY] [NOV] | 1.40% | |

| WED | 07:00 | GBP | Nationwide House Prices s.a. [MoM] [NOV] | -0.40% | -0.70% |

| WED | 08:45 | EUR | Italian PMI Manufacturing [NOV] | 53.10 | 53.00 |

| WED | 08:50 | EUR | French PMI Manufacturing [NOV F] | 57.50 | 57.50 |

| WED | 08:55 | EUR | German PMI Manufacturing [NOV F] | 58.90 | 58.90 |

| WED | 09:00 | EUR | Euro-Zone PMI Manufacturing [NOV F] | 55.50 | 55.50 |

| WED | 09:30 | GBP | Purchasing Manager Index Manufacturing [NOV] | 54.70 | 54.90 |

| WED | 13:30 | USD | Non-Farm Productivity [3Q] F | 2.30% | 1.90% |

| WED | 13:30 | USD | Unit Labor Costs [3Q F] [3Q] F | -0.20% | -0.10% |

| WED | 15:00 | USD | ISM Manufacturing [NOV] | 56.50 | 56.90 |

| WED | 15:00 | USD | Construction Spending [MoM] [OCT] | -0.40% | 0.50% |

| WED | 19:00 | USD | Fed's Beige Book [DEC] | ||

| WED | 00:30 | AUD | Trade Balance [Australian dollar] [OCT] | 2000M | 1760M |

| WED | 00:30 | AUD | Retail Sales s.a. [MoM] [OCT] | 0.40% | 0.30% |

| THU | 06:45 | CHF | Gross Domestic Product [YoY] [3Q] | 3.10% | 3.40% |

| THU | 06:45 | CHF | Gross Domestic Product [QoQ] [3Q] | 0.50% | 0.90% |

| THU | 08:15 | CHF | Retail Sales [Real] [YoY] [OCT] | 4.10% | |

| THU | 09:30 | GBP | Purchasing Manager Index Construction [NOV] | 51.30 | 51.60 |

| THU | 10:00 | EUR | Euro-Zone Gross Domestic Product [QoQ] [3Q] | 0.40% | 0.40% |

| THU | 10:00 | EUR | Euro-Zone Gross Domestic Product [YoY] [3Q] | 1.90% | 1.90% |

| THU | 10:00 | EUR | Euro-Zone Producer Price Index [MoM] [OCT] | 0.30% | 0.30% |

| THU | 10:00 | EUR | Euro-Zone Producer Price Index [YoY] [OCT] | 4.30% | 4.20% |

| THU | 12:45 | EUR | European Central Bank Rate Decision [DEC] | 1.00% | 1.00% |

| THU | 15:00 | USD | Pending Home Sales [MoM] [OCT] | -1.00% | -1.80% |

| THU | 15:00 | USD | Pending Home Sales [YoY] [OCT] | -24.90% | |

| THU | 01:00 | CNY | China Non-manufacturing PMI [NOV] | 60.50 | |

| THU | 02:30 | CNY | China HSBC Services PMI [NOV] | 56.40 | |

| FRI | 05:00 | EUR | German Retail Sales [MoM] [OCT] | 1.20% | -1.70% |

| FRI | 05:00 | EUR | German Retail Sales [YoY] [OCT] | 1.30% | 0.40% |

| FRI | 08:15 | CHF | Consumer Price Index [MoM] [NOV] | 0.10% | 0.50% |

| FRI | 08:15 | CHF | Consumer Price Index [YoY] [NOV] | 0.10% | 0.20% |

| FRI | 09:00 | EUR | Euro-Zone PMI Composite [NOV F] | 55.40 | 55.40 |

| FRI | 09:00 | EUR | Euro-Zone PMI Services [NOV F] | 55.20 | 55.20 |

| FRI | 10:00 | EUR | Euro-Zone Retail Sales [MoM] [OCT] | 0.20% | -0.20% |

| FRI | 10:00 | EUR | Euro-Zone Retail Sales [YoY] [OCT] | 1.00% | 1.30% |

| FRI | 12:00 | CAD | Net Change in Employment [NOV] | 20.0K | 3.0K |

| FRI | 12:00 | CAD | Unemployment Rate [NOV] | 7.90% | 7.90% |

| FRI | 13:30 | USD | Change in Private Payrolls [NOV] | 153K | 159K |

| FRI | 13:30 | USD | Change in Non-farm Payrolls [NOV] | 142K | 151K |

| FRI | 13:30 | USD | Unemployment Rate [NOV] | 9.60% | 9.60% |

| FRI | 15:00 | USD | ISM Non-Manufacutring Composite [NOV] | 54.70 | 54.30 |

| FRI | 15:00 | USD | Factory Orders [OCT] | -1.00% | 2.10% |

As noted it will be a big week for PMI (Purchasing Manager's Index) data releases. As can be seen in the table, results are due from the US, China, Japan, and throughout the EU. The results will provide a timely update, especially for the China and US results. I will be watching these two in particular very closely and will put out updates throughout the week. Consensus forecasts are picking a bit of an increase in China, and flat in the US, watch this space.

Australia will announce its 3rd quarter GDP result on Tuesday, with consensus picking slightly slower quarterly growth, and stronger year on year growth. Canada will also provide an update on its GDP results as will Switzerland and the wider EU. The EU is not expected to make an large revisions to its Q3 GDP results, but it will be worth a look, particularly on a country-by-country basis.

On the monetary policy front the European Central Bank meets on Thursday, and as usual the rate likely wont be moving, but it will be interesting to see what the ECB says given the rumblings in the EU sovereigns markets. As noted, the US Fed also releases the Beige book economic report this week, which will be interesting in light of the Fed's recent launch of QEII. Elsewhere in the world, Pakistan reviews rates on Monday, Thailand on Wednesday, and Indonesia on Friday; expecting only changes from Pakistan.

Apart from PMI, GDP, and monetary policy, some of the other interest data points out this week include: Japan industrial production (expected to slow), EU CPI and unemployment rate (expect little change), S&P Case-Shiller house price index (expect a monthly decline in Sep), US consumer confidence (expect an improvement), and of course US employment data for November with nonfarm payrolls expected to expand by a similar amount as October, and no change to the unemployment rate.

So as always, have a great week, watch out for surprises, and stay tuned for updates...

Sources

DailyFX www.dailyfx.com/calendar

Forex Pros www.forexpros.com/economic-calendar/

Forex Factory www.forexfactory.com/calendar.php

Bloomberg www.bloomberg.com

+various statistics websites and central bank websites for verification

Article Source: http://www.econgrapher.com/28nov-calendar.html

Friday, November 5, 2010

Top 5 Economics Graphs of the Week - 6 November 2010

This week we look at the PMI results for China and the US and reflect on their implications. Then we review the monetary policy decisions out over the past week including the announcement from the US FOMC. Then we wrap up with a look at the US employment figures for October, and the New Zealand employment stats for the September quarter.

1. China PMI

China saw a continued rebound in its manufacturing PMI figures for October, with the official CFLP figure rising to 54.7 from 53.8, and the the HSBC index rising to 54.8 from 52.9. Within the CFLP PMI index, the strong points were Production (57.1 vs 56.4), New orders (58.2 vs 56.3), and Inventory (49.5 vs 49.1), while the lower points were Employees (52.1 vs 52.4), and Supplier delivery (49.3 vs 50.4). So overall a reasonably good result, and reflects the continued strength in the Chinese economy - which is showing through into a higher stock market, with the SSE composite rising 15% in October.

2. US PMI

In the US, the October PMI result was also relatively positive with the main index rising to 56.9 from 54.4 driven by strength in new orders, production, and new export orders - with imports falling (a positive sign for net exports). While the non-manufacturing index also rose to 54.3 from 53.2, driven by strength in production, a large spike in prices, and back log of orders. So overall the October results for the US (unless there is some quirk to it) helps provide evidence or support for the non-double-dip scenario. So it is a positive, but at the same time the fundamentals are not quite there yet for economic growth to be anything more than subdued/baseline.

3. Monetary Policy Rates

In monetary policy the main event was the US FOMC announcing the $600 billion asset purchase program, to be implemented at a pace of $75 billion per month. The other major moves were tightening of monetary policy rates in Azerbaijan (100bps), Vietnam (100bps), Australia (25bps), and India (25bps), and loosening of monetary policy rates in Iceland (75bps), and Latvia (12.5bps). Meanwhile other banks held rates due to low inflationary pressures and a desire to keep stimulatory monetary policy conditions to aid the economic recovery e.g. US, EU, UK, Japan.

4. US Nonfarm payrolls

Back to the US, the October nonfarm payrolls pleasantly surprised to the upside, with 151k jobs added in October vs consensus 60k and previous -95k (revised to -41k). Private payrolls grew 159k in October vs 64k in September. Average hourly earnings crept up slightly 0.2% and the average work week was 34.3 hours vs 34.2 in September. So overall, as with the PMI results another good result for the US, a positive from the perspective that it's not going down, but there's still a long way to go before the ground lost during the crisis can be recovered.

5. NZ Employment situation

In New Zealand the Q3 employment report saw the unemployment rate dip to 6.4% from a revised 6.9% in the June quarter. Total persons employed grew by 22k, with part-time jobs increasing 12k and full-time jobs expanding 10k. Across the sectors the jobs growth was relatively broad based with most sectors adding jobs. The figure reflects the progress, albeit slow, being made in the New Zealand economic recovery, but the subdued nature is showing through with deleveraging playing through. One major challenge for New Zealand is the high exchange rate which will impact on net exports, but a key driver of that is weakness in the US dollar. In terms of monetary policy the RBNZ has likely finished tightenings for the year, but will likely continue early next year as the recovery unfolds.

Summary

So we saw relatively strong PMI results in China which showed the economy is still running strong in the middle kingdom. The US also showed strong results in its PMI stats, providing some comfort against the double-dip scenario, but not yet being able to offer more than a subdued, sub-trend economic growth outcome. In monetary policy the major banks are holding tight but other banks are acting as the case demands, with several emerging economies opting to tighten or normalise monetary policy as inflation risks trump growth risks. In employment, the US showed a strong result in October, and New Zealand also showed a pretty good result in Q3. So overall it's a scene of economic recovery, but all is not yet clear and well.

Sources:

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Yahoo Finance finance.yahoo.com & Institute for Supply Management www.ism.ws

3. CentralBankNews.info www.centralbanknews.info

4. US Bureau of Labor Statistics www.bls.gov

5. Statistics New Zealand www.stats.govt.nz

Article Source: http://www.econgrapher.com/top5graphs6nov.html

1. China PMI

China saw a continued rebound in its manufacturing PMI figures for October, with the official CFLP figure rising to 54.7 from 53.8, and the the HSBC index rising to 54.8 from 52.9. Within the CFLP PMI index, the strong points were Production (57.1 vs 56.4), New orders (58.2 vs 56.3), and Inventory (49.5 vs 49.1), while the lower points were Employees (52.1 vs 52.4), and Supplier delivery (49.3 vs 50.4). So overall a reasonably good result, and reflects the continued strength in the Chinese economy - which is showing through into a higher stock market, with the SSE composite rising 15% in October.

2. US PMI

In the US, the October PMI result was also relatively positive with the main index rising to 56.9 from 54.4 driven by strength in new orders, production, and new export orders - with imports falling (a positive sign for net exports). While the non-manufacturing index also rose to 54.3 from 53.2, driven by strength in production, a large spike in prices, and back log of orders. So overall the October results for the US (unless there is some quirk to it) helps provide evidence or support for the non-double-dip scenario. So it is a positive, but at the same time the fundamentals are not quite there yet for economic growth to be anything more than subdued/baseline.

3. Monetary Policy Rates

In monetary policy the main event was the US FOMC announcing the $600 billion asset purchase program, to be implemented at a pace of $75 billion per month. The other major moves were tightening of monetary policy rates in Azerbaijan (100bps), Vietnam (100bps), Australia (25bps), and India (25bps), and loosening of monetary policy rates in Iceland (75bps), and Latvia (12.5bps). Meanwhile other banks held rates due to low inflationary pressures and a desire to keep stimulatory monetary policy conditions to aid the economic recovery e.g. US, EU, UK, Japan.

4. US Nonfarm payrolls

Back to the US, the October nonfarm payrolls pleasantly surprised to the upside, with 151k jobs added in October vs consensus 60k and previous -95k (revised to -41k). Private payrolls grew 159k in October vs 64k in September. Average hourly earnings crept up slightly 0.2% and the average work week was 34.3 hours vs 34.2 in September. So overall, as with the PMI results another good result for the US, a positive from the perspective that it's not going down, but there's still a long way to go before the ground lost during the crisis can be recovered.

5. NZ Employment situation

In New Zealand the Q3 employment report saw the unemployment rate dip to 6.4% from a revised 6.9% in the June quarter. Total persons employed grew by 22k, with part-time jobs increasing 12k and full-time jobs expanding 10k. Across the sectors the jobs growth was relatively broad based with most sectors adding jobs. The figure reflects the progress, albeit slow, being made in the New Zealand economic recovery, but the subdued nature is showing through with deleveraging playing through. One major challenge for New Zealand is the high exchange rate which will impact on net exports, but a key driver of that is weakness in the US dollar. In terms of monetary policy the RBNZ has likely finished tightenings for the year, but will likely continue early next year as the recovery unfolds.

Summary

So we saw relatively strong PMI results in China which showed the economy is still running strong in the middle kingdom. The US also showed strong results in its PMI stats, providing some comfort against the double-dip scenario, but not yet being able to offer more than a subdued, sub-trend economic growth outcome. In monetary policy the major banks are holding tight but other banks are acting as the case demands, with several emerging economies opting to tighten or normalise monetary policy as inflation risks trump growth risks. In employment, the US showed a strong result in October, and New Zealand also showed a pretty good result in Q3. So overall it's a scene of economic recovery, but all is not yet clear and well.

Sources:

1. CFLP www.chinawuliu.com.cn & Markit/HSBC www.markiteconomics.com & Yahoo Finance finance.yahoo.com

2. Yahoo Finance finance.yahoo.com & Institute for Supply Management www.ism.ws

3. CentralBankNews.info www.centralbanknews.info

4. US Bureau of Labor Statistics www.bls.gov

5. Statistics New Zealand www.stats.govt.nz

Article Source: http://www.econgrapher.com/top5graphs6nov.html

Subscribe to:

Posts (Atom)