Before looking at the charts, it's worth noting the title "a policy-driven, multispeed recovery". This is an adroit description of how things are unfolding. For example, emerging markets versus developed economies; and within developed economies there's even different paces e.g. UK (slow, and subdued) vs Australia (relatively unscathed, and recovering faster).

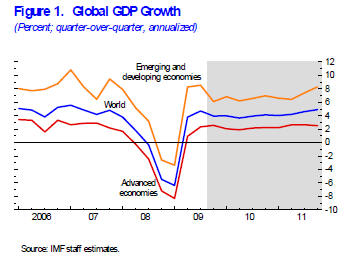

1. Global GDP Growth

The first chart in the report is the old global growth outlook chart. On GDP growth, the IMF revised it's forecast for the global economy to 3.9% in 2010, vs a previously forecast 3.1%. There really isn't anything surprising about it for those who've been paying attention.

The advanced economies took the biggest hit, and will return to growth eventually, albeit potentially lower then the average prior to the crisis. Then there's the emerging markets who did take a hit to a greater or lesser extent, but are set to recover back to high growth levels.

"In most advanced economies, the recovery is expected to remain sluggish by past standards, whereas in many emerging and developing economies, activity is expected to be relatively vigorous, largely driven by buoyant internal demand."

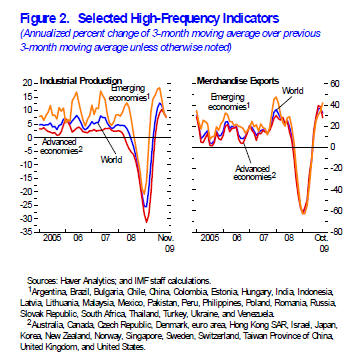

2. High-Frequency Indicators

The next chart to look at from the report is the high-frequency indicators: industrial production, and merchandise exports. Global trade is a great metric to monitor for gauging the level of economic activity in the world economy.

On trade, many countries have seen a recovery in trader off the lows or a "normalisation", indeed China has already reached the same levels it saw just prior to the crisis. Meanwhile industrial production, for now is underpinned by stimulus measures and the inventory cycle.

"In advanced economies, the beginning of a turn in the inventory cycle and the unexpected strength in U.S. consumption contributed to positive developments. Final domestic demand was very strong in key emerging and developing economies, although the turn in the inventory cycle and the normalization of global trade also played an important role."

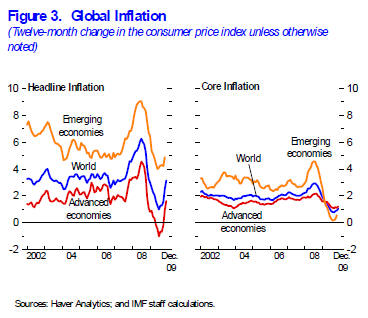

3. Global Inflation

For those that follow the Econ Grapher updates, it's no surprise to see the trends in inflation in the charts below. There has been a marked turnaround in headline inflation, boosted in part by a low comparison value, and similarly by the commodities cycle. What's also interesting to note though is that core inflation has also bottomed out and started to turn upwards.

The inflation piece of the puzzle is an interesting one, and while some (e.g. PIMCO) are suggesting deflation, others are warning about inflation. This plays into how monetary and fiscal policy will evolve over the next year, and it will be a difficult dilemma for policy makers to find the middle path.

"In the advanced economies, headline inflation is expected to pick up from zero in 2009 to 1¼ percent in 2010, as rebounding energy prices more than offset slowing labor costs. In emerging and developing economies, inflation is expected to edge up to 6¼ percent in 2010, as some of these economies may face growing upward pressures due to more limited economic slack and increased capital flows."

Before summing up it's worth reviewing what the IMF sees as the key Upside, and Downside risks.

Upside:

-"The reversal of the confidence crisis and the reduction in uncertainty may continue to foster a stronger-than-expected improvement in financial market sentiment and prompt a larger-than-expected rebound in capital flows, trade, and private demand."

-"New policy initiatives in the United States to reduce unemployment could provide a further impetus to both U.S. and global growth."

Downside:

-"A premature and incoherent exit from supportive policies may undermine global growth and its rebalancing."

-"Impaired financial systems and housing markets or rising unemployment in key advanced economies may hold back the recovery in household spending more than expected."

-"Rising concerns about worsening budgetary positions and fiscal sustainability could unsettle financial markets and stifle the recovery by raising the cost of borrowing for households and companies."

-"Rallying commodity prices may constrain the recovery in advanced economies."

Summary

The update to the World Economic Outlook has provided some interesting data and projections, as well as thoughts to consider. The upward revisions to the growth outlook are promising in terms of where 2010 may go, but it's clear by looking at the balance of risks, that there is still much more that can go wrong than right at this point.

In terms of how this ties in with investment strategy, it confirms a reasonably widely held view that emerging markets will outperform developed markets in the coming years (at least on an economic growth basis). It also adds to the macro risk-reward picture over the next couple of years in terms of how the recovery will evolve, and what may derail it (and therefore what to keep an eye out for).

Source:

1, 2, 3. IMF World Economic Outlook (WEO) Update http://www.imf.org/external/pubs/ft/weo/2010/update/01/index.htm

Article Source: http://econgrapher.site1.net.nz/WEOupdate-jan2010.html

No comments:

Post a Comment

What do you think?